Home Value Forecast

The Timeline of a Turnaround

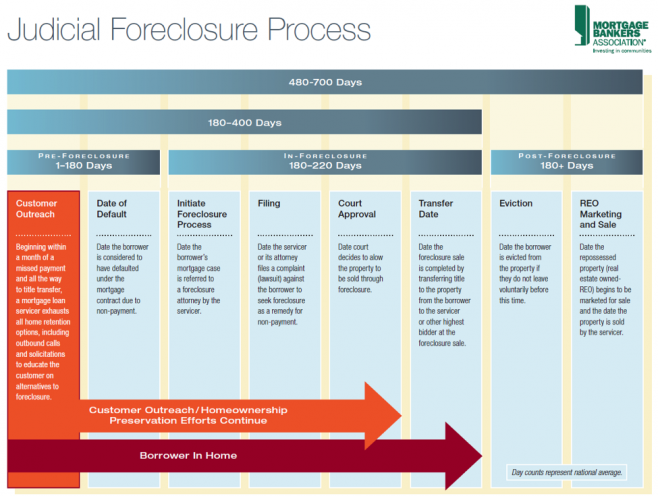

In the U.S., state foreclosure laws are either judicial or non-judicial, as has been reported in previous Home Value Forecast updates. Each state has its own specific rules and timelines.

In judicial states, a foreclosure is a court proceeding that has specific, court ordered steps along the way. Twenty two states use judicial procedures as the primary way to foreclose, including Connecticut, Delaware, Florida, Hawaii, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, New Jersey, New Mexico, New York, North Dakota, Ohio, Oklahoma, Pennsylvania, South Carolina, South Dakota, Vermont, and Wisconsin.

In non-judicial states, foreclosure requirements are established by state statute with no court intervention. State specific rules and timelines are followed, resulting in a faster foreclosure process.

Below is an example of a judicial foreclosure timeline as provided by the Mortgage Bankers Association:

So, how does this impact housing values? Two years ago, much of the bad news was centered on California, a non-judicial state. Foreclosures were driving down prices, there were massive losses, and people were wondering where the bottom of the market was and when it would be reached. In response, banks moved swiftly to cut losses, peak foreclosure activity came and went, and now markets are on the rebound. In fact, eight of our top ten metros for this month are in California.

In judicial states, like Florida and Illinois, the foreclose process can take up to two years. Unlike California, which tore off the foreclosure Band-Aid quickly, Florida and Illinois have been slowly peeling it away. In these states there are still high ratios of foreclosure sales and hefty foreclosure discounts, which in turn are limiting any real recovery. Because of this, all of our bottom ten metros are in Florida or Illinois.

In this month’s CBSA Winners and Losers, we take a closer look at how the foreclosure discount is impacting our Top and Bottom Metros.

CBSA Winners and Losers

Each month, Home Value Forecast ranks the single family home markets in the top 200 CBSAs to highlight the strongest and weakest metros with regard to a number of leading real estate market based indicators.

The ranking system is purely objective and is based on directional trends. Each indicator is given a score based on whether the trend is positive, negative, or neutral for that series. For example, a declining trend in active listings would be positive, as will be an increasing trend in average price. A composite score for each CBSA is calculated by summing the directional scores of each of its indicators. From the universe of the top 200 CBSAs, we highlight the CBSAs each month which have the highest and lowest composite scores.

The tables below show the individual market indicators which are being used to rank the CBSAs along with the most recent values and the percent changes. We have color-coded each of the indicators to help visualize whether it is moving in a positive (green) or negative (red) direction.

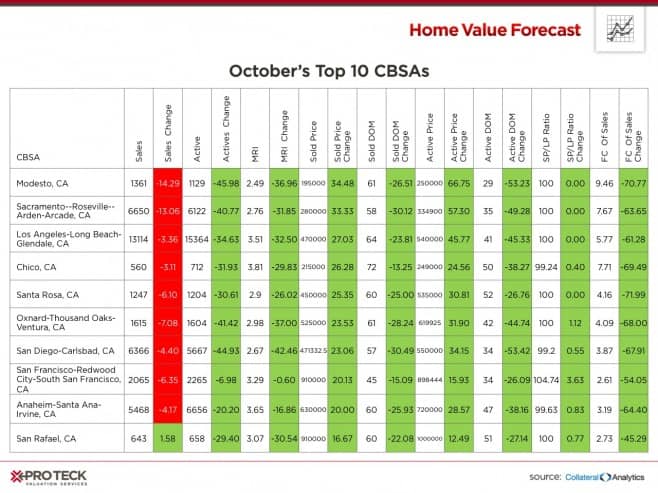

Top 10 CBSAs

Our top ten CBSA list this month is dominated by California, but all are showing impressive numbers. Each have less than four months of inventory and are averaging more than 20 percent year over year appreciation. Of importance is the foreclosure as a percent of sales – all are under 10 percent. Supply-demand market fundamentals have returned, which should lead to a sustainable recovery. All of these CBSAs are in non-judicial states.

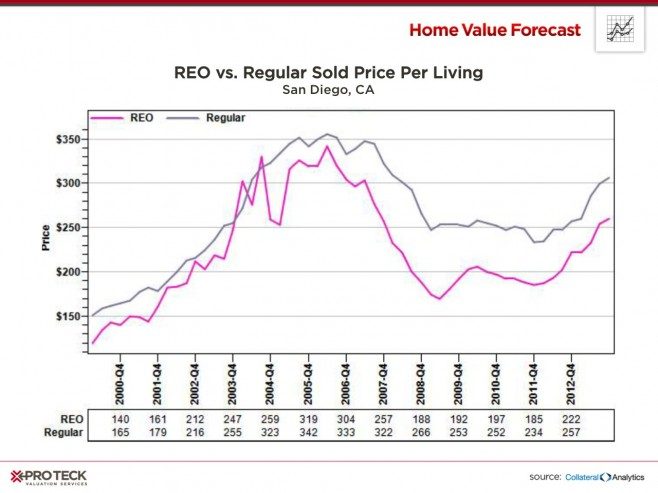

The below image graphically shows the REO discount in San Diego, CA, one of our top 10 metros:

As you can see, the discount was at its highest in Q4 2008, when it was nearly 30 percent. The spread has steadily tightened as the bulk of foreclosures has made it through the system. As of Q4 2012, the spread was under 14 percent and it is still tightening. Regular prices have also rebounded, now trending less than 12 percent below the all-time high.

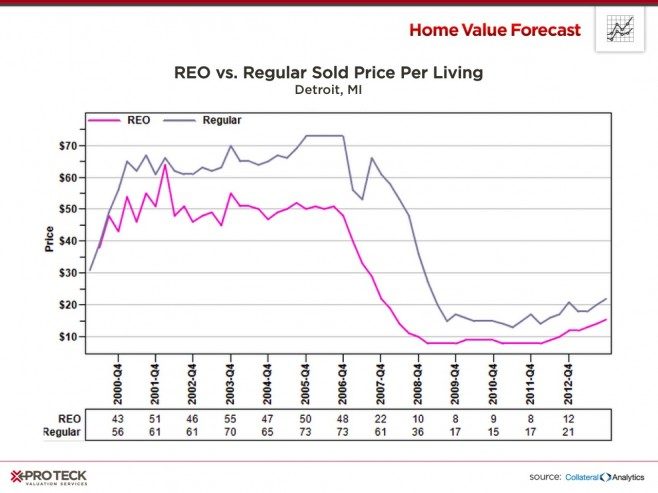

One metro not mentioned in our top ten is Detroit. Much has been made of Detroit’s price appreciation over the last year, and many indexes that focus exclusively on year over year sale price change have them as one of their hottest markets. Home Value Forecast considers price appreciation along with eight other different market attributes in its ranking, providing a more forward and holistic look at the relative strength of housing markets. Because foreclosures still make up a large percentage of sales in the Detroit metro, we still see it as a “weak” market that will have to work through the foreclosures and REO’s before seeing median home prices within earshot of it’s peak.

Comparing the REO to Regular sales graph, below, for Detroit, versus San Diego, above, brings this squarely into focus.

Detroit REO discount is still more than 30 percent and regular home prices are running 70 percent below 2006 highs, making Detroit have more in common with our bottom ten metros. We do appreciate the positive signs in Detroit, but there is still more work to be done before the market is healthy again.

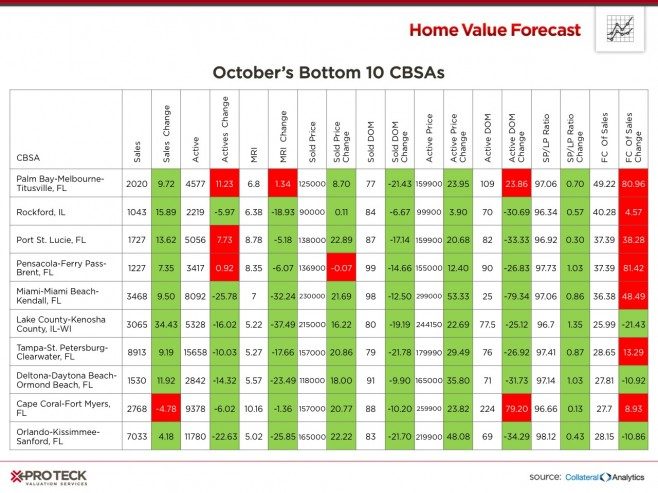

Bottom 10 CBSAs

It’s hard to sustain a market turnaround when 25-50 percent of sales are foreclosures. When foreclosures represent a significant share of total sales and their discounted prices pull down the prices of non-distressed sales, it is known as the “contagion effect.” This is what is happening in our bottom ten CBSAs this month.

Even though other market fundamentals are looking good, such as recent price appreciation and shrinking inventories, foreclosures are still playing a major part in holding these real estate markets back. A stable market cannot return until foreclosures play a less active role in the market.

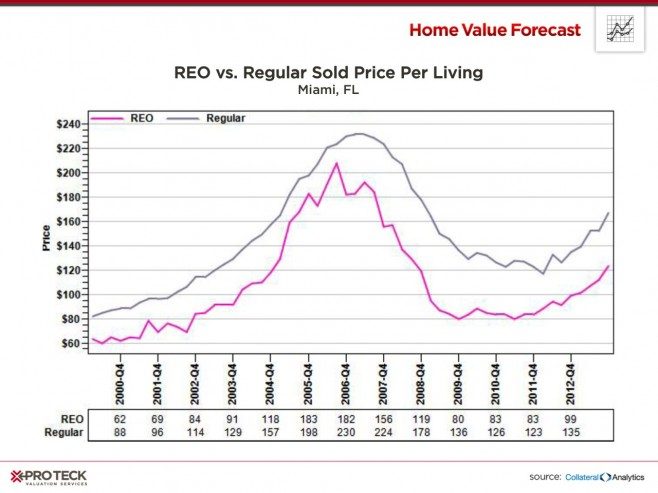

Below is a graph of the foreclosure discount in Miami, FL, one of our bottom 10 markets:

As you can see, the bottom of the market was two years after that of San Diego, CA, mostly because of the judicial system dragging out the foreclosure process. While the spread between regular and REO sales has diminished, it is still above 25 percent and is still holding back the price appreciation we have seen in non-judicial markets like San Diego. Where San Diego is now within 12 percent of its peak, Miami remains 28 percent below its all-time high.

We will keep an eye on all these markets as foreclosures finally return to historical levels.