Home Value Forecast

2013 Year in Review

All of us at Home Value Forecast would like to wish you the very best during the holiday season and a happy New Year!

As 2013 comes to an end, Home Value Forecast looks back at trends over the last 12 months in a number of residential real estate categories. 2013 delivered big improvements in the housing market, but a closer look shows that the recovery varies widely from one metropolitan area to the next.

This December, we see a continued recovery in many parts of the country, particularly western and sand states, while housing markets in other areas, like Florida, continue to struggle. Our review of the year also reminds us of how the Colorado flooding and other natural disasters can have a short-term negative impact on overall housing recovery, temporarily impacting activity as homes are repaired and affected by changing flood zones and insurance costs.d

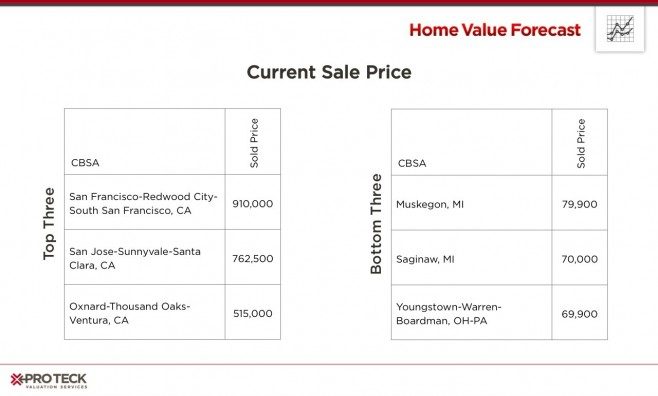

Current Sale Price

For December 2013, we see a large difference between median prices across the country, just look at the $820,000 spread between San Francisco and Youngstown. The recovery is well underway in this traditionally expensive metro area where housing prices are up more than 15 percent for the quarter, versus down 4 percent in Youngstown.

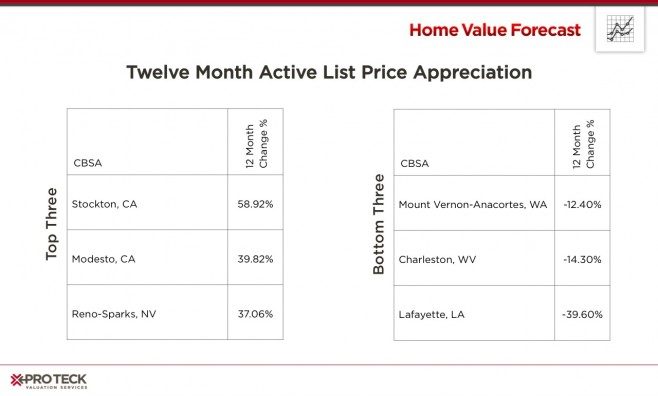

Twelve-Month Active List Price Appreciation

“Active price” is the median price a home is listing for at a moment in time. We like to look at list price as a good reflection of market health, because it takes into account people’s perceptions of where prices are headed. Again, California is at the top of the list.

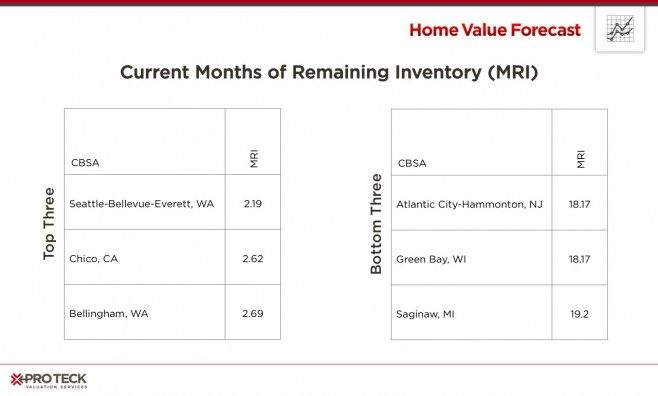

Current Months of Remaining Inventory (MRI)

MRI is another indicator that shows how “hot” a market is at a particular time. MRI equals the amount of households on the market divided by the number that sell per month. If an area has a high MRI (let’s say 10 months), it means that the market is saturated — a buyer’s market. If MRI is low (2–3 months) then it becomes a seller’s market. A “balanced” market will have approximately six months of inventory at any given time.

As of today, Washington State and California are seeing the most limited supply of housing for sale, with our top 10 in lowest MRI all being from those two states.

Twelve-Month Sales Price Appreciation

Sales price appreciation is a good thing, but the statistic by itself can be deceiving. Our top three all had 35+ percent appreciation for the year, yet all were decimated by the housing crisis. For example, while the Deltona/Daytona CBSA is up almost 60% this year to an average sold price of $130,000, it still has a ways to go to top the $212,200 average it hit in the 3rd Quarter of 2006. What these numbers reflect is that the market has responded to the bargains that are out there, lowering inventory and driving up prices. The result is a housing market that went from overvalued to undervalued before realigning to reflect supply/demand fundamentals.

CBSA Winners and Losers

Each month, Home Value Forecast uses a number of leading real estate market-based indicators to rank the single family home markets in the top 200 CBSAs to highlight the strongest and weakest metros.

The ranking system is purely objective and is based on directional trends. Each indicator is given a score based on whether the trend is positive, negative or neutral for that series. For example, a declining trend in active listings would be positive, as will be an increasing trend in average price. A composite score for each CBSA is calculated by summing the directional scores of each of its indicators. From the universe of the top 200 CBSAs, we highlight each month the CBSAs which have the highest and lowest composite scores.

The tables below show the individual market indicators that are being used to rank the CBSAs along with the most recent values and the percent changes. We have color coded each of the indicators to help visualize whether it is moving in a positive (green) or negative (red) direction.

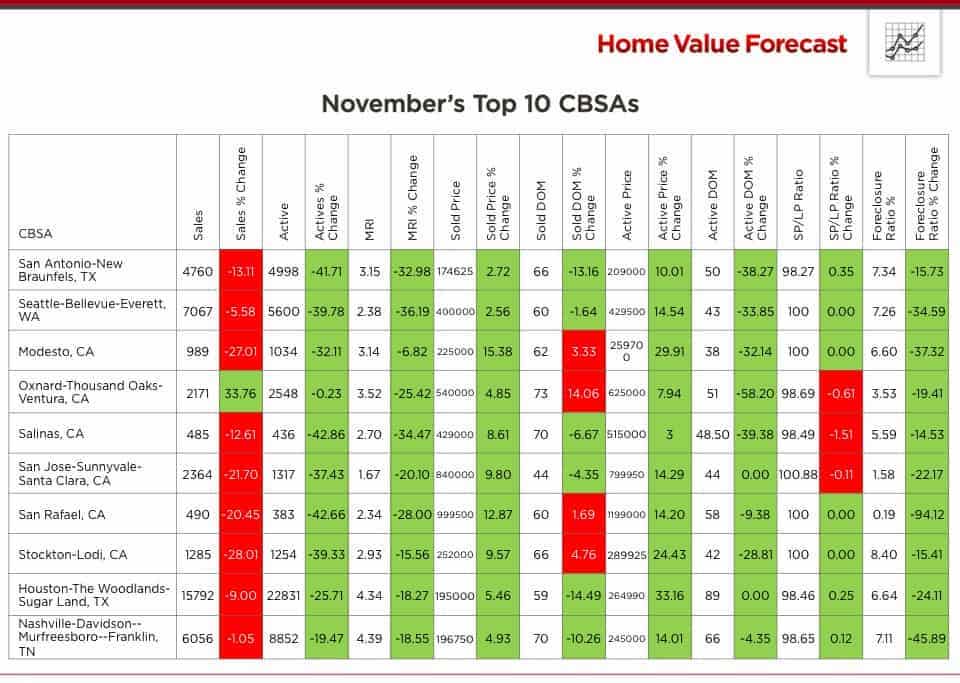

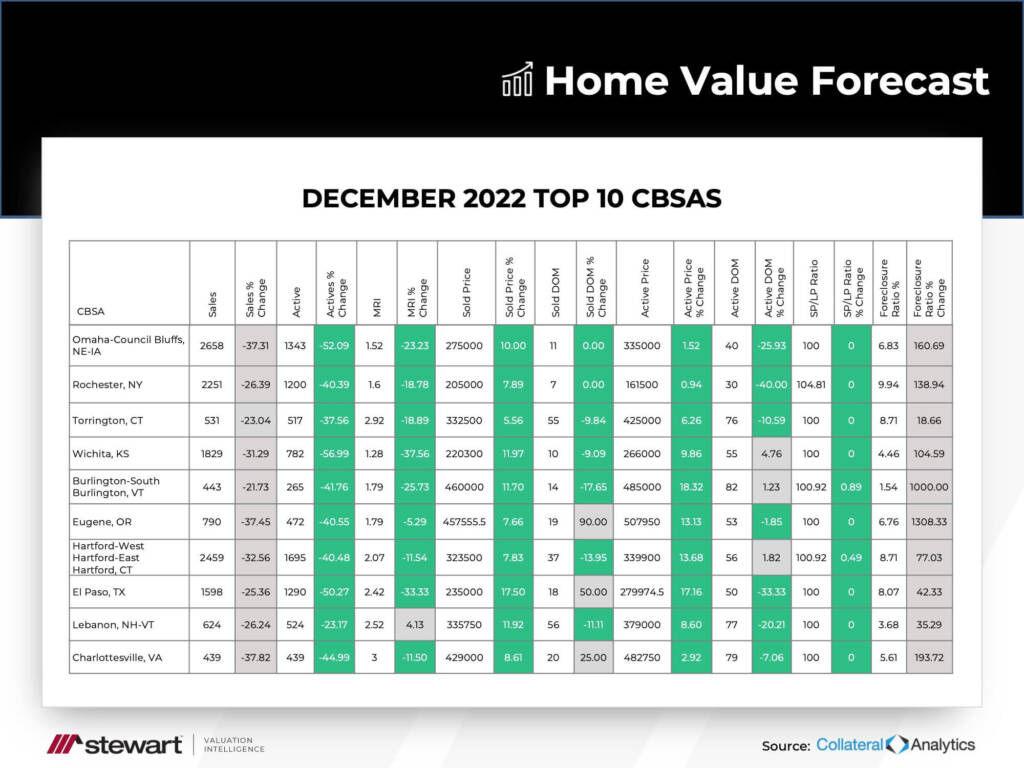

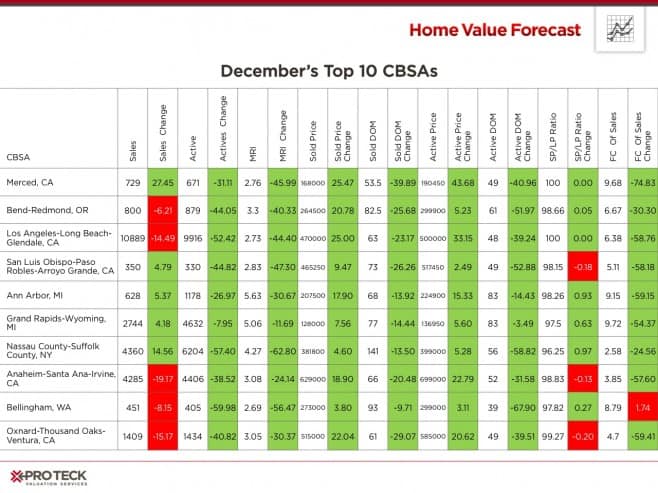

Top 10 CBSAs

The western United States is well represented again in our top 10, with seven metros from California, Oregon and Washington. Foreclosure as a percentage of sales is a very important indicator at Home Value Forecast — as you can see, none of our top 10 metros have more than 10 percent of sales from foreclosure, and most have seen a 50+ percent reduction in the number. Also housing stock as represented by MRI are between 2 and 5 months, indicating a hot market.

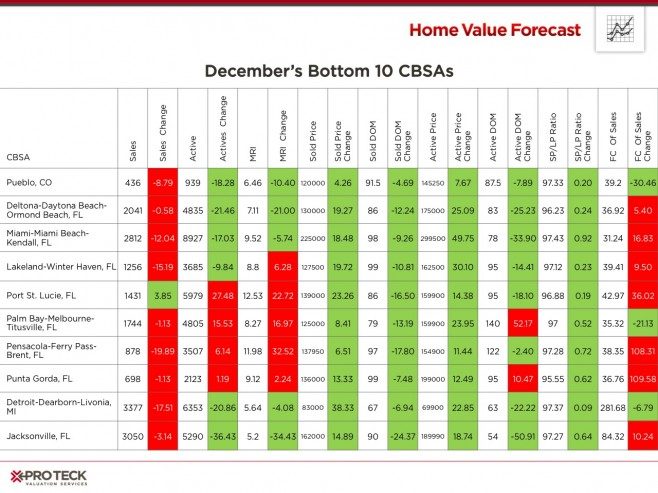

Bottom 10 CBSAs

As we discussed in our last update, it’s hard to sustain a market turnaround when 35+ percent of sales are foreclosures, as is the case in Detroit and many Florida metros. When foreclosures represent a significant share of total sales and their discounted prices pull down the prices of non-distressed sales, it is known as the “contagion effect.” This is what is happening in our bottom 10 CBSAs this month.

A new entrant to our bottom 10 is Pueblo, CO. Pueblo was hit hard by flooding in September of this year, and it is showing in the market (Grand Junction, CO also was ranked as a “weak” market, but did not appear in our bottom 10). In all, more than 18,000 homes were damaged and 2,000 destroyed by the flooding in Colorado — we will be watching to see if the effects are seen in other metro markets.